ICT trading strategy explained

ICT — short for Inner Circle Trader — is one of the more polarising methodologies in retail forex trading. Some traders swear by it. Others dismiss it as overcomplicated, or worse, as a system built more on mystique than mechanics. The truth sits somewhere more practical than either camp admits.

The methodology was developed by Michael Huddleston, who began publishing trading content under the ICT brand in the early 2010s. Over time, the approach accumulated a substantial following, particularly among traders who felt that conventional technical analysis — trendlines, indicators, pattern recognition — was leaving too much unexplained. ICT offered a different frame: that price movements are not random or purely sentiment-driven, but are instead the result of deliberate institutional behaviour that retail traders can learn to read.

Whether that framing is entirely accurate is a separate debate. But the concepts themselves — many of which draw on established ideas in market microstructure — are worth understanding on their own terms. And for forex traders specifically, some of them translate quite directly into practice.

What ICT trading is and where it comes from

Huddleston's core premise is that large institutional players — banks, hedge funds, central bank intermediaries — move price in predictable ways, and that those movements leave footprints visible on the chart. ICT methodology is, at its base, an attempt to identify those footprints before price completes its move.

The approach draws selectively from earlier concepts. Smart Money Theory, which holds that institutional order flow dominates retail sentiment, underpins most of the ICT framework. Wyckoff accumulation and distribution logic is present, though rarely credited directly. What Huddleston added was a specific vocabulary and a structured sequence for reading price — one that gives traders a repeatable process rather than a loose collection of ideas.

That vocabulary is part of what makes ICT initially difficult to approach. Terms like "order blocks," "fair value gaps," and "liquidity sweeps" sound proprietary. Some of them are. But strip away the branding and many of these concepts describe market behaviours that institutional traders and market microstructure researchers have discussed for decades. The packaging is new. The underlying logic, largely, is not.

Core concepts behind the ICT methodology

Order blocks are where most traders start. In ICT terms, an order block is the last opposing candle before a significant price move — the final bearish candle before a strong bullish impulse, for instance. The theory holds that institutional orders were placed in that zone, and that price will return to it before continuing in the original direction. Traders use these zones as potential entry points.

Fair value gaps are equally central. When price moves so sharply that it leaves a gap between three consecutive candles — specifically, when the wicks of the first and third candles do not overlap — ICT traders treat that gap as an imbalance. The expectation is that price will eventually retrace to fill it. This is not unique to ICT; imbalance concepts appear in futures trading and order flow analysis broadly. But ICT gives it a specific name and a specific application sequence.

Then there is liquidity. ICT traders think in terms of where stop-losses cluster — above recent highs, below recent lows — because institutional players need liquidity to fill large orders. A "liquidity sweep" describes price briefly breaching those levels to trigger stops before reversing. Spotting these sweeps, in theory, helps traders avoid being on the wrong side of them.

How ICT traders analyse the market

ICT analysis begins with the higher timeframes and works down. A trader might start on the weekly or daily chart to identify the prevailing market structure — whether price is making higher highs and higher lows, or the reverse — and then drop to the four-hour or one-hour chart to locate relevant order blocks and fair value gaps within that structure. The entry itself might be refined on the fifteen-minute or five-minute chart.

This top-down process is not unique to ICT, but the methodology is unusually specific about what to look for at each level. At the macro level, the focus is on what ICT calls "premium and discount zones." Price trading above the midpoint of a defined range is considered premium — theoretically expensive. Below the midpoint is discount. ICT traders generally look to buy in discount zones and sell in premium ones, aligning with the broader institutional bias they've identified.

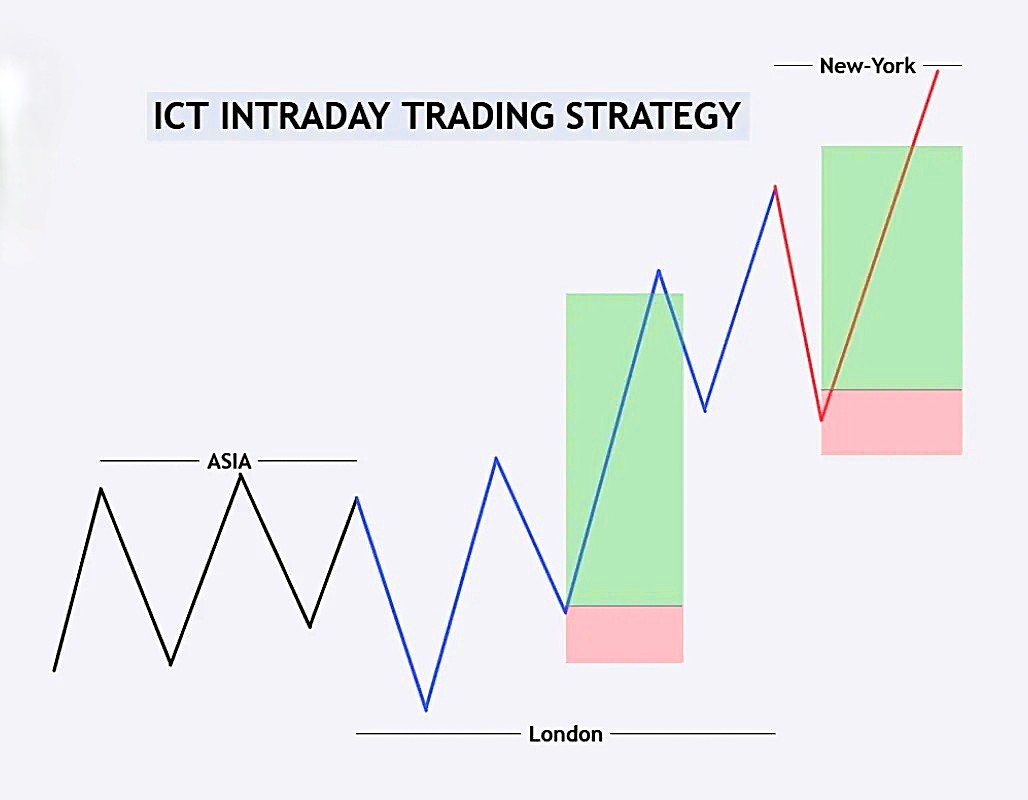

Time also plays a larger role in ICT than in most retail frameworks. Certain trading sessions — particularly the London open and New York open — are considered high-probability windows because institutional activity tends to concentrate there. The concept of "kill zones," specific one-to-two-hour windows around these opens, reflects that. It is one of the more practically applicable ideas in the methodology, and one that often trips up traders who ignore session timing entirely.

Applying ICT concepts in the forex market

Forex suits the ICT framework reasonably well, partly because the currency market is dominated by institutional players. The Bank for International Settlements estimates that a substantial share of daily forex volume flows through a small number of major dealer banks — exactly the kind of participants ICT theory centres on.

Consider a practical sequence on EUR/USD. A trader identifies a bearish daily structure — lower highs, lower lows. On the four-hour chart, they locate an order block formed just before the most recent sharp leg down. Price has since retraced back into that zone. On the one-hour chart, a fair value gap sits within the order block. The trader waits for price to enter the gap during the London kill zone, then looks for a lower-timeframe entry signal — a shift in market structure on the five-minute chart, for example — before placing the trade with a stop above the order block.

That sequence — higher timeframe bias, institutional zone, session timing, lower timeframe entry — is roughly how a systematic ICT trader would approach the setup. Execution varies between traders, but that logical chain is consistent across most ICT-influenced strategies.

Risk management within ICT is less formalised than the entry process. Most practitioners apply standard position sizing principles — risking a fixed percentage of account equity per trade, typically one to two percent.

Limitations and criticisms of the ICT approach

The most honest criticism of ICT is also the most structural: many of its concepts are difficult to define objectively. What qualifies as a valid order block versus a random candle? At what point does a retracement become an invalidation? ICT provides guidelines, but the application frequently comes down to discretion — which means two traders can look at the same chart and see entirely different setups.

That subjectivity creates a backtesting problem. Strategies built on pattern recognition that requires human judgment are notoriously difficult to validate statistically. A trader may recall the setups that worked and unconsciously discount the ones that did not. This is confirmation bias operating in a framework that, ironically, presents itself as structured and rule-based.

There is also the question of the foundational narrative. The idea that institutional players deliberately engineer liquidity sweeps to trap retail traders is compelling, but it is not empirically verified in the way that, say, central bank intervention signals are documented. Some of the behaviour ICT describes is real — stop-hunting and liquidity-driven price movements are observable phenomena. Whether they occur as deliberately and as consistently as the methodology implies is harder to establish.

None of this means ICT lacks utility. But traders who adopt it wholesale, without stress-testing the concepts against their own data, tend to run into trouble.

Is ICT right for you?

That depends almost entirely on how a trader learns and how much screen time they are willing to invest. ICT is not a plug-and-play system. The framework requires absorbing a significant amount of conceptual material before any of it clicks in real market conditions — and even then, developing the pattern recognition takes months of consistent chart work.

Traders who prefer rule-based, algorithmic, or indicator-driven approaches will likely find ICT frustrating. The discretionary element is not a bug in the methodology; it is central to how it functions. For traders who are comfortable reading price action and making judgment calls in real time, that same discretion becomes an advantage.

There is also a practical consideration around trading sessions. ICT concepts tend to perform best during high-liquidity windows — London and New York in particular. Traders operating in time zones that make those sessions difficult to access will need to adapt, and the framework does not always translate cleanly to Asian session conditions, where institutional flow is thinner.

For traders willing to put in the analytical work, test concepts individually rather than all at once, and apply disciplined risk management regardless of the setup quality, ICT offers a genuinely different lens on price. Whether that lens improves outcomes depends on the trader, not the methodology.